1. What Is a Boundary Setting Method? What Role Does It Play in Carbon Inventory?

In plain terms, a boundary setting method is the "accounting rule" for inventory boundaries — it establishes clear allocation rules and ensures methodological consistency from the outset. It primarily determines two things:

- Which entities should be included in the carbon inventory (i.e., the scope of the organizational boundary)

- Whether the emissions from included entities are accounted for at 100%, or allocated proportionally

Under prevailing international practices, common boundary setting methods typically revolve around concepts such as "equity share" or "control (financial/operational)." ISO 14064-1 also adopts this same framework as the methodological basis for organizational boundary design.

The reason boundary setting methods matter is that they simultaneously affect the following three dimensions:

- Overestimation or underestimation of total emissions

If a joint venture's emissions are accounted for at 100% under the operational control approach but only at 30%–40% under the equity share approach, a single entity can significantly affect total emissions and emission hotspots (high-emission items). - Distortion of year-over-year comparisons

If the operational control approach was used last year but the equity share approach is adopted this year, the emissions trend actually reflects "the result of a methodology change" rather than operational improvement or deterioration. - Confusion in category classification and data responsibility

Under different methods, the same facility may directly affect whether a particular activity or emission source should be included in the company's inventory. Once the inclusion scope changes, the corresponding data responsibilities and category classifications must be adjusted accordingly.

When setting inventory boundaries, companies should be mindful of the differing requirements from two major regulatory authorities. Entities regulated by the Ministry of Environment should define boundaries based on the geographic scope covered by the "control number," and account for each emission source using the operational control approach. The Financial Supervisory Commission (FSC), on the other hand, requires that boundaries align with the consolidation scope of "financial statements." Although the FSC does not impose a single mandatory method for attributing subsidiary emissions (such as financial control, operational control, or equity share approach), companies must ensure internal consistency in their calculation logic.

2. Control Approach & Equity Share Approach

When conducting a carbon inventory using the international standard ISO 14064-1:2018, there are two main directions for setting organizational boundaries: the control approach and the equity share approach. The control approach can be further divided into two assessment methods: operational control and financial control.

2-1. Operational Control: Who Manages the Site and Day-to-Day Operations?

An entity that has the authority to introduce and implement operating policies (e.g., operational procedures, equipment operation, etc.) is generally considered to have operational control.

Quick summary: Whoever can decide how things are done and managed on site typically has operational control.

2-2. Financial Control: Who Manages Finances and Business Policies?

If an entity can direct the financial and operating policies of an operation and derives the majority of economic benefits (e.g., controls budget and investment decisions), it is generally considered to have financial control.

Quick summary: Whoever can decide how money is spent, how the business is run, and captures the majority of economic benefits typically has financial control.

Unlike the control approach, which determines inclusion based on "whether control exists," the equity share approach uses a "proportional (%)" concept to allocate emissions. This method is particularly suited to joint ventures, associates, or complex investment structures, as it more closely reflects the risks and benefits actually borne by the company.

2-3. Equity Share Approach

A company accounts for emissions from an operation based on its equity share / economic interest; economic interest reflects the company's entitlement to the risks and rewards of that operation.

A simple example:

- Joint venture annual emissions: 1,000 tCO₂e

- Our company's equity stake: 40%

- Under the equity share approach, our company accounts for: 400 tCO₂e

Quick summary: Your share of the investment determines your share of the emissions.

Current Regulations and Practices in Taiwan

In Taiwan, when companies adopt a boundary setting method recognized under the international standard ISO 14064-1:2018, the operational control approach is the most commonly chosen option. This is because it enables clearer division of responsibilities, more efficient acquisition of emissions data, and — since the company has direct authority over equipment upgrades and process optimization — best reflects carbon reduction performance. However, given that circumstances vary across companies, relying solely on the operational control approach may not fully capture the economic interests and emission attribution actually borne by the company. Therefore, companies should evaluate whether alternative consolidation approaches, such as the equity share approach, may be more appropriate based on their specific needs and management objectives, in order to improve the reasonableness and comparability of their inventory results.

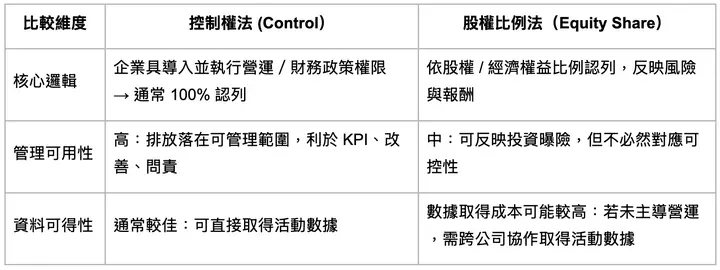

3. Control Approach vs. Equity Share Approach: Differences, Pros, and Cons

- Control approach: Looks at "who manages day-to-day operations / finances" → With operational / financial control, emissions are typically accounted for at 100%

- Equity share approach: Looks at "what is the ownership stake" → Emissions are accounted for proportionally

4. What Happens If You Choose the Wrong Method? Four Common Impacts

When the wrong boundary setting method is chosen, the most common consequence is that "results are questioned, requiring recalculation or methodological restructuring."

- Impact on the inventory subject

For the same joint venture or investment structure, adopting a different boundary setting method may shift some entities from "full inclusion" to "proportional inclusion." Once the method changes, total emissions, emission hotspots, and the identification of significant emission sources will change accordingly. - Impact on year-over-year comparability, with increased verification costs

If boundary setting methods are changed back and forth between years, emissions results are effectively built on different calculation bases. This undermines consistent interpretation of emissions trends, making it difficult to determine whether changes stem from "operational performance" or "a change in boundary method." During verification and audits, such inconsistencies are also more likely to trigger follow-up questions and requests for additional explanations. - Impact on data responsibility and ease of data collection

The boundary setting method affects not only "which entities are included" but also which emission sources and activity data each entity is responsible for collecting and substantiating. This can result in: omitting items that should be included, or double-counting items that should not be, ultimately compromising the completeness and verifiability of the final emissions data.

5. How to Accurately Select a Boundary Setting Method and Effortlessly Execute a Carbon Inventory Project?

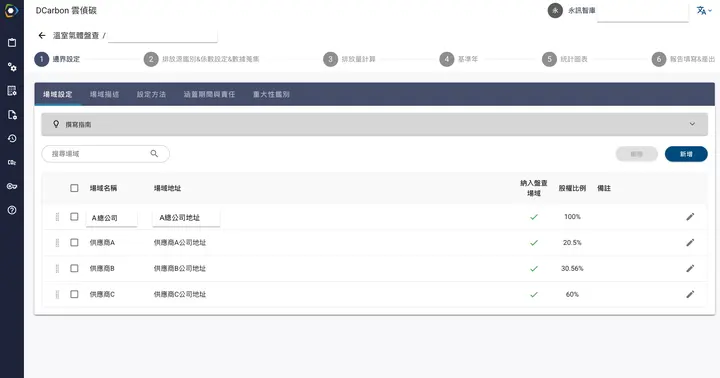

In addition to correctly selecting the boundary setting method that best suits your organization, a user-friendly software system that supports various boundary setting methods will certainly be a powerful asset for completing your carbon inventory with ease.

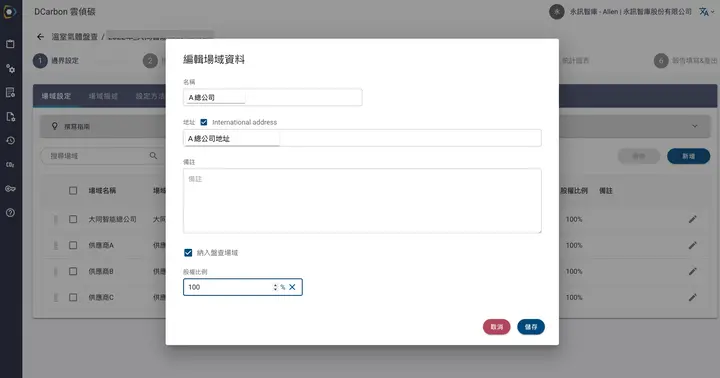

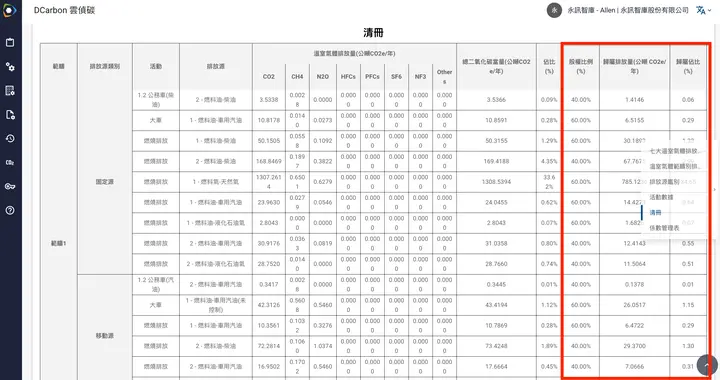

Each facility within the organization can have its equity share ratio configured individually

Recently, in addition to the existing control approach, Sustaihub has launched a brand-new "Equity Share Approach" calculation module to better meet diverse user needs and assist your company not only in completing the inventory project but also in passing third-party verification with ease. Users can use the feature shown in the image above to set the equity share ratio for each facility, allowing the system to automatically calculate the "attributed total emissions" for each facility based on its respective ratio, clearly presenting the post-allocation emissions results for every facility.

Review the post-allocation emissions results