What Is the FY2026 (115) ESG Evaluation? A New Regime of 75 Indicators Across Three Dimensions

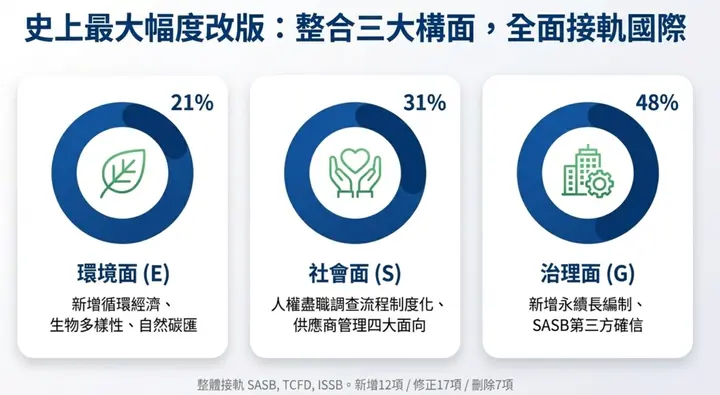

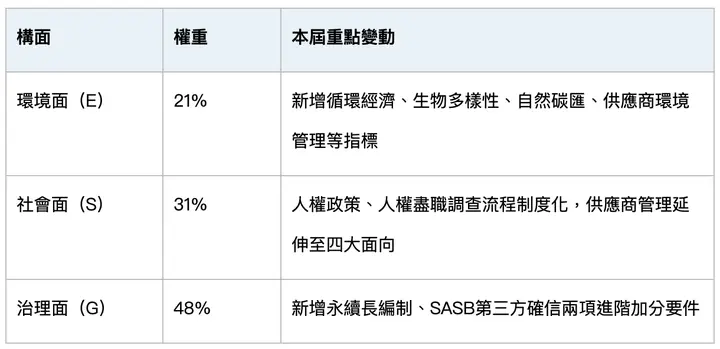

From FY2026 (year 115 ROC) onward, the Taiwan Stock Exchange officially transforms the former "Corporate Governance Evaluation" into the "ESG Evaluation". The previous four dimensions are consolidated into three — Environment (E), Social (S) and Governance (G) — with 75 indicators in total, weighted 21% E, 31% S and 48% G. The first cycle brings the largest change in years: 12 additions, 17 revisions, 7 deletions and 5 question-type adjustments, with the overall direction far closer to SASB, TCFD and ISSB (source: TWSE Corporate Governance Center ESG Evaluation Portal).

For listed companies this is not an incremental revision — it is a structural shift in evaluation logic. If the sustainability report does not map precisely to the new indicators during drafting, newly added items such as E-14 Biodiversity or G-30 Chief Sustainability Officer become almost impossible to add once the report reaches the June layout and English-translation stage. Deep review must be completed before the FY2025 report is filed on 31 August to protect the points you could have earned.

Six Key Points at a Glance

Once the sustainability report draft is complete, work through the following six review actions in order:

- Point 1 – Indicator mapping: map every section of the draft to the 75 ESG Evaluation indicators and create a three-level gap tag.

- Point 2 – New-indicator inventory: prioritise the four newly added indicators that are most frequently overlooked.

- Point 3 – Environment (E) top-up: verify completeness of GHG, water, waste, energy and biodiversity disclosures.

- Point 4 – Social (S) top-up: close gaps on the three external documents required for human-rights due diligence.

- Point 5 – Governance (G) bonus items: pursue advanced bonus items such as G-30 Chief Sustainability Officer and G-33 SASB third-party assurance.

- Point 6 – Submission-timeline control: back-solve from the 31 August filing date to confirm the available days for gap closure, layout and translation.

Each point is expanded below.

Point 1: What Is the First Step After the Sustainability Report Draft Is Complete?

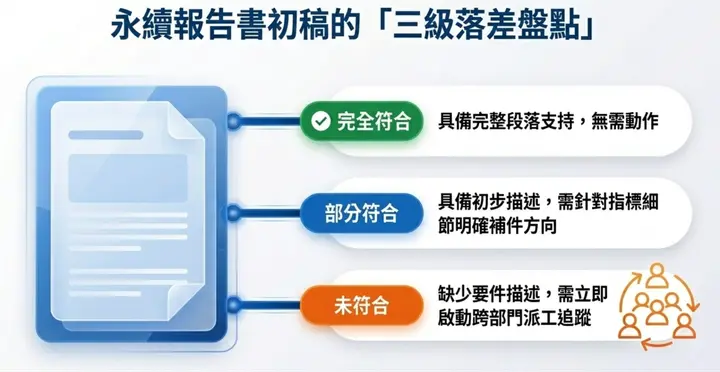

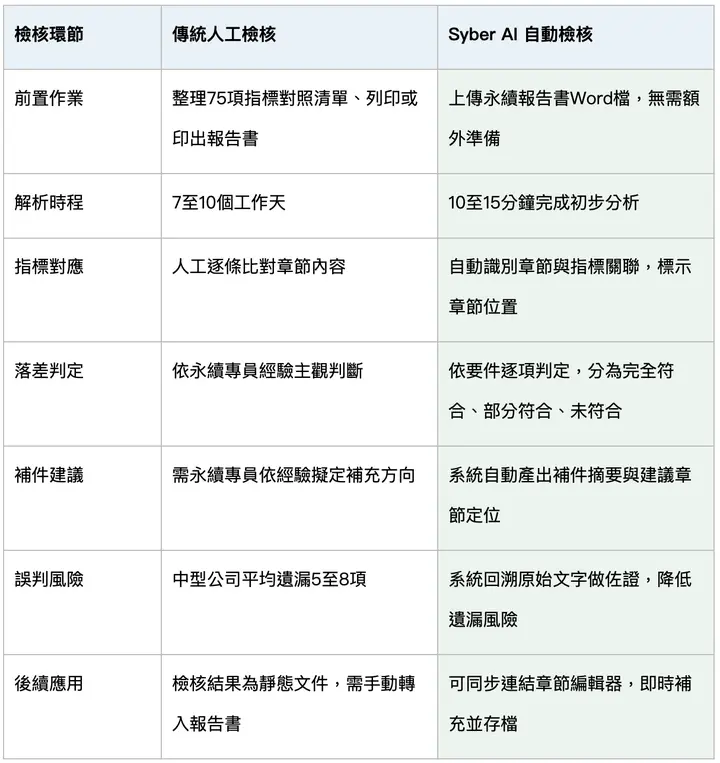

The first step after the draft is finished is to map the content against the 75 indicators of the 2026 ESG Evaluation — identifying which indicators are backed by existing sections, which lack content, and which are mentioned but fall short of the bonus-item requirements. Based on Sustaihub's advisory case data, a ~200-page mid-cap listed company sustainability report takes an average of 7–10 working days to review manually against 75 indicators, with a non-trivial omission rate.

We recommend creating three tagging columns on the tracking sheet:

- Fully compliant: clear paragraphs, data or policy documents that meet the indicator's requirements.

- Partially compliant: the topic is mentioned but lacks quantitative data, time-series or explicit targets.

- Non-compliant: no relevant content is found in the draft at all.

This gap table is the starting point for every downstream remediation task. We recommend listing indicator number, draft chapter, compliance state, responsible unit and planned close-out date to enable cross-department tracking.

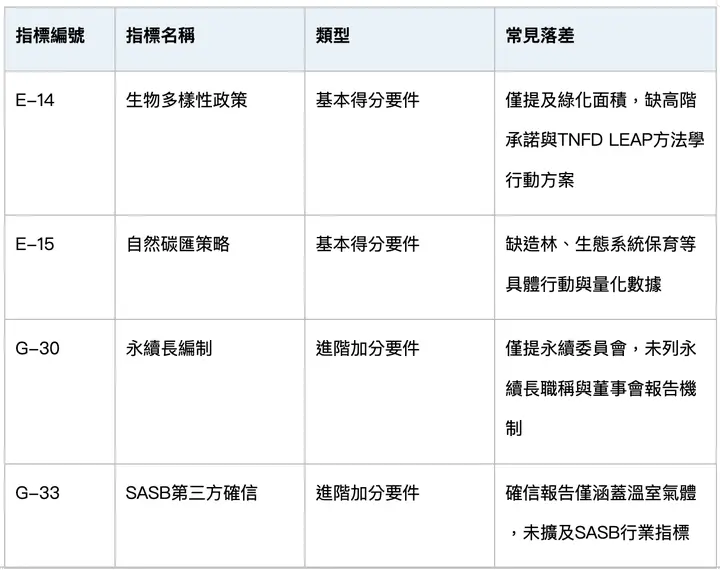

Point 2: Which Four New Indicators in the 2026 ESG Evaluation Are Most Often Missed?

Of the 12 newly added indicators in the first ESG Evaluation cycle, the following four are most commonly missed in the draft — because the former Corporate Governance Evaluation had no equivalent items, and sustainability teams tend to reuse the old structure:

- E-14 Biodiversity policy or commitment: requires a senior-level commitment document, ideally aligned with the TNFD LEAP methodology.

- E-15 Natural carbon-sink strategy and measures: directly tied to the carbon-neutrality pathway; requires a clearly scoped inventory.

- G-30 Chief Sustainability Officer: requires a formal appointment record and a mechanism for regular board-level sustainability reporting.

- G-33 SASB disclosure with third-party assurance: an advanced bonus item that requires lead time to book third-party assurance.

The first two require senior-level commitments and alignment with international frameworks; the latter two involve personnel decisions and budget allocation. Their common trait: the sustainability team cannot complete any of them alone. The later you start, the harder the gap is to close.

Point 3: Which Environment (E) Indicators Are Most Often Written Incompletely?

New and revised indicators on the environment side cluster around GHG, water, waste, energy and biodiversity. The three below are the ones most commonly "mentioned but incomplete":

- E-2 GHG inventory: Scope 1, 2 and 3 must be explicitly disclosed, with assurance level and assurance provider identified.

- E-5 Total waste volume disclosure and circular-economy policy: beyond total tonnage, the circular-economy or waste-management policy must be described.

- E-6 Energy-use disclosure: renewable and non-renewable energy must be broken out separately, with an annual trend.

The most common omission pattern is disclosing only current-year totals without a three-year trend or target value, which downgrades the indicator to "partially compliant". When closing the gap, fill in the historical data at the same time so you do not have to rework it next year.

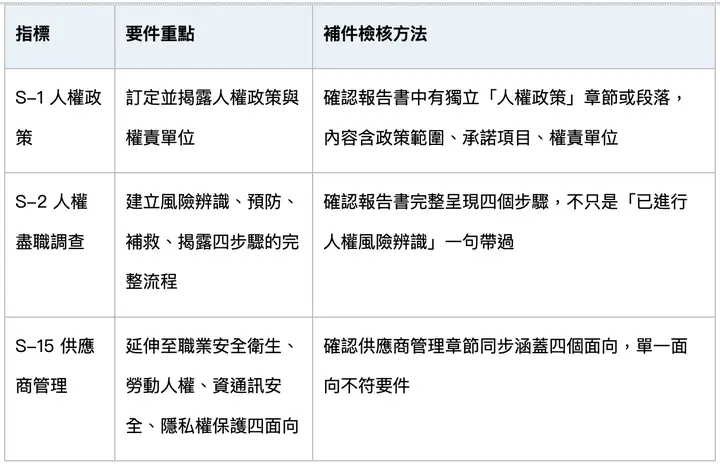

Point 4: What Are the Review Checkpoints for Social (S) Human-Rights Due Diligence?

The core change on the social side is the institutionalisation of S-1 Human-rights policy and S-2 Human-rights due-diligence process and execution. These indicators are not satisfied by a single paragraph of text — at minimum the company needs three external documents:

Close the gap in three steps:

- Human-rights policy: drafted by compliance or the sustainability team, approved by the board, and published externally.

- Risk identification: start from high-risk suppliers (high migrant-worker ratio, prior labour disputes) and build a tiered list.

- Remediation and grievance channels: integrate into existing employee and supplier communication platforms — no new system required.

The social side also has one newly added indicator that is easy to miss: "friendly measures for marriage, childbirth or family care". This does not need senior-level commitment, but HR must supply the specific programme and usage data — include it in the remediation list.

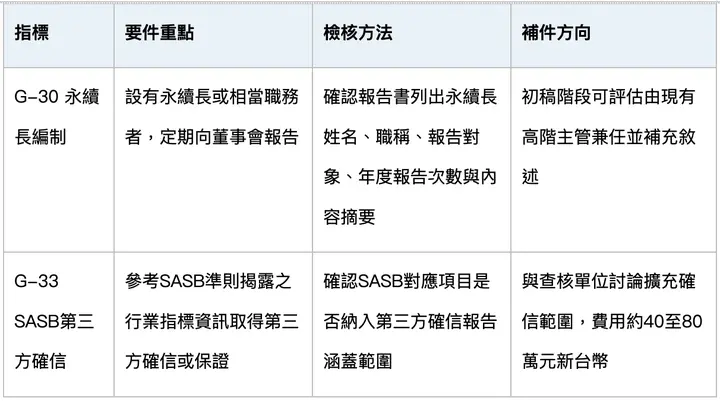

Point 5: What Are the Governance (G) Bonus-Item Checkpoints?

The two advanced bonus items on the governance side are the easiest ways to differentiate in the 2026 ESG Evaluation:

- G-30 Appointing a Chief Sustainability Officer with regular board reporting: requires a formal appointment record and board meeting minutes.

- G-33 Disclosing SASB industry metrics and obtaining third-party assurance: reserve lead time for the third-party provider, typically 2–3 months.

If you start on these two items only after the report is published, you are already too late. If this cycle is not feasible, at least state in the sustainability report the planned execution timeline and next-year targets so evaluators see the commitment.

Beyond the bonus items, confirm that existing indicators reflect regulatory updates — for example, the independent-director rule that no single director may serve more than three consecutive terms requires matching against the current board composition.

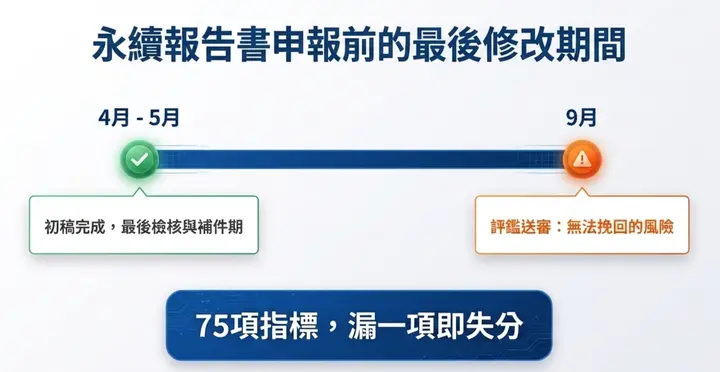

Point 6: How Should You Back-Solve the 2026 ESG Evaluation Submission Timeline?

This point is the most easily overlooked and the most consequential. Back-solve the timeline as follows:

- April – May | Draft complete; kick off the 75-indicator gap review.

- End of May | Cross-department remediation complete; final copy submitted for internal review.

- June – July | Layout design, English translation, third-party assurance.

- 31 August | File the FY2025 sustainability report with the TWSE.

- From September | ESG Evaluation review window opens; remediation is no longer possible.

In other words, the actual remediation window between draft completion and final copy is only about 4–6 weeks. If remediation requires board approval or third-party assurance, build the board-meeting dates into the schedule as well.

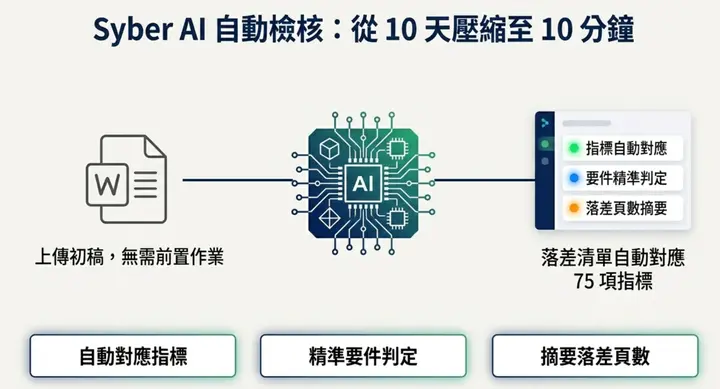

How Syber AI Accelerates ESG Evaluation Review: Upload a Word File and Get Automatic Indicator Mapping

Syber AI's operating logic is straightforward: the company uploads a sustainability report in Word, the system parses the chapter structure, determines which ESG Evaluation indicators each chapter maps to, and at the indicator level produces a three-level judgement — "fully compliant", "partially compliant" or "non-compliant" — with a gap summary and reference page numbers.

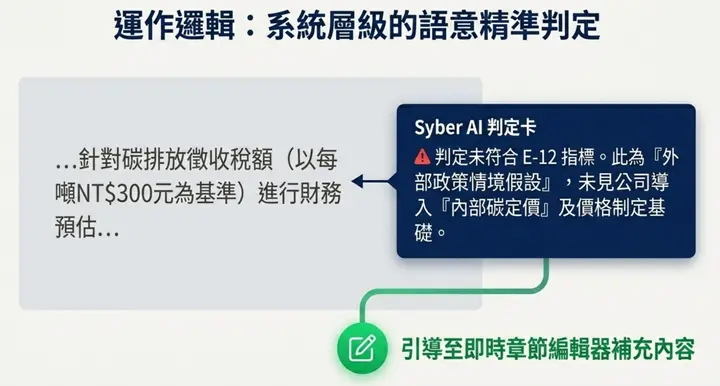

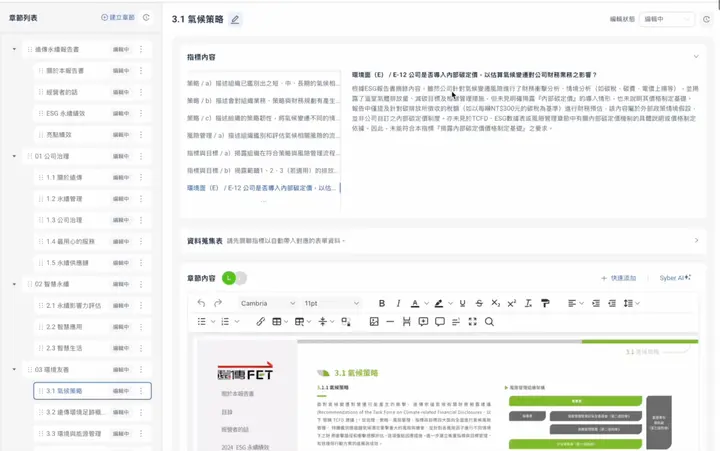

Using one client's uploaded sustainability report as an example, clicking E-12 "Has the company introduced an internal carbon price?" produces the following Syber AI judgement:

The company has performed financial impact analysis and scenario analysis for climate change risk (covering carbon tax, carbon fee and electricity-price rises), and has disclosed GHG emissions, reduction targets and management measures. However, the introduction of an "internal carbon price" is not explicitly disclosed, nor is the price-setting basis. The report only mentions financial estimates using the tax amount imposed on carbon emissions (e.g. NT$300/tonne carbon tax), which is an external policy-scenario assumption rather than an internal carbon-pricing scheme defined by the company. Therefore, the requirement to "disclose the internal carbon-price setting basis" is not met.

This judgement tells the sustainability team three things:

- Where the gap is: the internal carbon-pricing scheme is not disclosed.

- Why it is non-compliant: an external carbon-tax scenario is treated as internal carbon pricing.

- How to close it: add the pricing basis, scope of application and actual use case to the TCFD or risk-management chapter.

Syber AI also ships a chapter editor — remediation content can be written directly into the corresponding chapter without switching tools. The judgement logic covers all 75 indicators; the system compares each requirement line by line and will not miss details even when the indicator text is long.

Manual Review vs Syber AI Automated Review: Seven-Stage Comparison

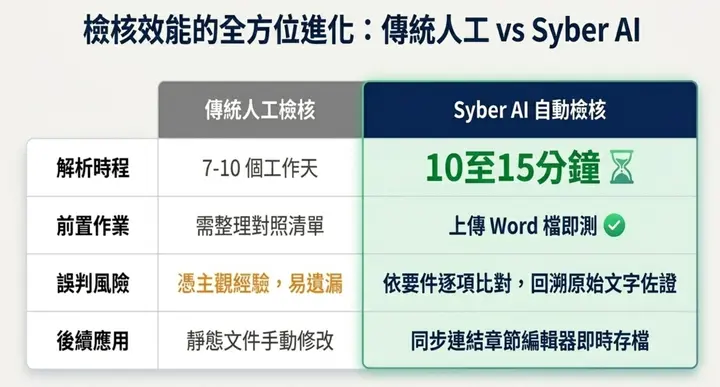

For a 150-page sustainability report, manually reviewing 75 indicators takes 7–10 working days on average; Syber AI can complete the initial review and output a gap list within the same day. The table below compares the two approaches across each stage:

The time saved can be redirected to items that genuinely require cross-department remediation — human-rights due diligence, biodiversity policy and other indicators that need senior-level decisions and cross-functional collaboration.

Sustaihub Viewpoint

Between April and June each year, most sustainability teams are busy submitting drafts for internal review, revising content and confirming internal processes. The first ESG Evaluation's new indicators are not always fully reviewed at the draft stage — but once the report is published and the September evaluation window opens, there is almost no room for remediation.

Syber AI is designed to move this review work from "manual page-by-page cross-referencing" to "system-generated gap list", so that sustainability teams and consultants can spend their time on the remediation decisions that truly require professional judgement, rather than repetitive comparison work.