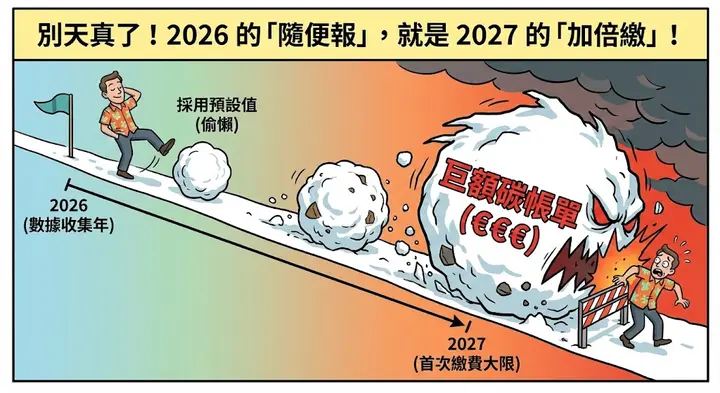

Introduction: 2026 Turning Point — Why Enterprises Can No Longer Afford to Wait

Many Taiwanese exporters mistakenly believe that since "CBAM certificate purchases start in 2027," they can relax in 2026. However, import emissions throughout 2026 will serve as the calculation basis for the first batch of certificates, with the first annual declaration and certificate submission deadline being September 30, 2027. Inaccurate data or reliance on default values could inflate certificate requirements, translating into high carbon costs.

Therefore, immediate action is essential. Establishing an actual measurement data system not only ensures compliance but also optimizes pricing to maintain competitiveness in the EU market.

1. 2026 Regulatory Updates: From Reporting-Only to Actual Payment Obligations

Upon entering the definitive phase, the core CBAM mechanism shifts from quarterly operations to annual settlement, with key changes as follows:

- Certificate Purchase Timeline: Official sales begin on February 1, 2027. Importers must purchase corresponding certificates based on 2026 full-year emissions.

- First Settlement Deadline: Annual reports must be submitted and certificates surrendered by September 30, 2027.

- Price Linkage: Certificate prices are linked to EU ETS weekly auction averages. Higher carbon emissions mean greater financial pressure on exports.

This is a "current year accumulation, next year settlement" model. Higher emissions mean greater certificate demand and rising export costs. Taiwanese enterprises should collect data early to help EU importers calculate precise embedded emissions.

2. Farewell to the "Default Value Fantasy": Actual Data Is the Only Cost Control Tool

During the transition period, many enterprises relied on "default values," but after 2026, default values will be designed as "conservative and overestimated" calculations, intended to penalize enterprises lacking data governance capabilities.

- punitive markup: Default values will apply annual markups based on exporting country average intensity: 10% markup in 2026, 20% in 2027.

- Advantages of Actual Values: Only actual data verified by Accredited Verifiers can bypass this 10% punitive cost.

- Financial Chain Effect: Relying on default values makes pricing uncompetitive, causing clients to switch to competitors with low-carbon data.

3. Carbon Price Deduction Practices: How to Avoid Overpaying?

With Taiwan’s carbon fee system soon to be implemented, exporters often ask: "If we’ve already paid local carbon fees, can we avoid double taxation under CBAM?" The answer is yes. The EU provides a deduction mechanism for "double taxation," but the prerequisite is proving that carbon prices have been actually paid and have a direct correspondence with the declared product emissions.

4. Practical Analysis: 5 Steps to Complete the CBAM Declaration Process

Based on the latest Omnibus Regulation (EU) 2025/2083, Taiwanese exporters should implement the following steps:

- Product CN Code Determination: Confirm whether products such as cement, steel, aluminum, fertilizers, and hydrogen are included.

- 50-Tonne Mass Threshold: This is the latest benefit! If an EU importer's total annual regulated goods are below 50 tonnes, declaration and certificate obligations are waived (not applicable to electricity and hydrogen).

- Data Collection and Boundary Definition: Collect in-plant process, energy, and upstream emission data. When collecting internal and external emission data, note that the EU has strict requirements for "calculation scope and activity data sources." In this "low tolerance for error" environment, minor formula deviations or batch errors from traditional Excel manual operations can trigger chain reactions affecting final declaration credibility and cost deduction rights.

- Precise Embedded Emission Calculation: Monitor and allocate according to the latest EU methodology. If using a "hybrid approach (actual + default)," attention must be paid to the complexity of weighted calculations.

- Annual Report Generation: Submit through the CBAM Registry. 2026 data will undergo final verification by September 2027.

Conclusion: When AI Meets CBAM — From Anxiety to Automated Data Governance

The core challenge of the CBAM definitive phase lies in "data governance." Transforming emissions into verifiable, traceable "assets" is the ticket for enterprises to survive in the green trade era.

Traditional Excel cannot handle complex audit trails and changing regulatory markups. We recommend adopting digital tools such as DCarbon Cloud Carbon System for digitized collection, calculation, and document generation. Perfecting your data system in 2026 will not only avoid cost shocks in 2027 but also secure long-term advantages in the EU market!