Sustainability reports have become a mandatory disclosure document for listed companies. After companies file their reports by the end of August each year, regulatory authorities initiate the review mechanism. If the report content does not comply with the "Operating Procedures for Listed Companies to Prepare and File Sustainability Reports," companies may be required to correct report content, submit process improvement plans, undergo training, or even face impacts on their corporate governance ratings. This article summarizes the "Sustainability Report Review Mechanism and Common Deficiencies" briefing published by TWSE and TPEx, compiling common deficiencies in report preparation to help companies conduct early self-examination and ensure compliance.

Who May Be Subject to Review?

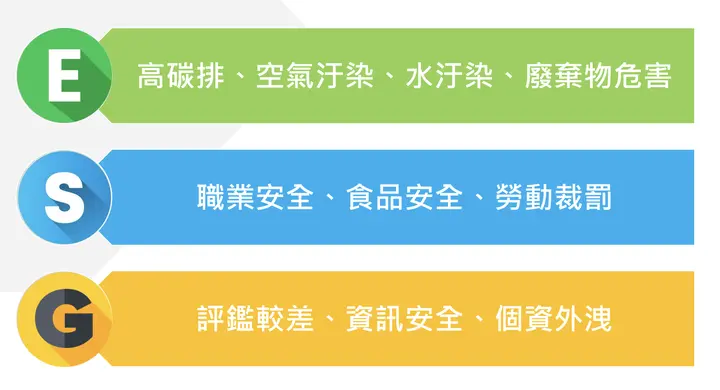

In principle, sustainability reports prepared by all listed companies will undergo review by TWSE or TPEx at least once every five years to ensure that disclosed content complies with relevant regulations and guidelines. In addition to regular reviews, regulatory authorities will adopt a Risk-Based Approach based on the ESG high-risk characteristics shown below to strengthen reviews of specific companies.

For example, if a company was a high carbon emitter in the environmental dimension in the previous year, or was penalized for violating the Labor Standards Act in the social dimension, or experienced an information security incident in the governance dimension, regulatory authorities will reference such risk indicators as criteria for selecting review targets.

ESG High-Risk Characteristics in Three Dimensions:

Source: TWSE, TPEx (2024/11) Review Mechanism and Common Deficiencies

Review Content and Focus Areas

The key content reviewed by TWSE and TPEx for sustainability reports is mainly divided into general review and specific topics. Below is a summary of important considerations for each:

- General Review:

- Must refer to GRI 2 General Disclosures requirements to disclose all relevant indicators; indicators GRI 2-1 to 2-5 cannot be omitted, and reasons must be provided for other undisclosed indicators

- Must refer to GRI 3 Material Topics to explain the process for determining material topics and disclose identification results

- Must refer to Article 4-1 of Operating Procedures for Preparing and Filing Sustainability Reports to disclose climate information

- If the company's industry has published "Sustainability Disclosure Indicators" for that specific industry, all indicators must be fully disclosed

- Specific Topics:

- For material topics, companies must refer to the corresponding GRI topic-specific standards.

Common Report Deficiencies

To help companies enhance disclosure quality, Sustaihub has compiled the 13 common sustainability report deficiencies listed by regulatory authorities, along with specific report examples. Companies can use this article to review their sustainability report content item by item to avoid deficiencies due to incomplete disclosure.

(1) Not Referencing the Latest GRI Standards

Common Deficiency: Not stating that the report was prepared with reference to the latest GRI Standards. If a company mistakenly uses outdated GRI indicators, regulatory authorities will require the report to be recompiled!

Better Disclosure Practice: Companies should refer to the current version of GRI - GRI 2021 version, and state the referenced standards in the report.

Report Example:

Source: China Airlines 2023 Sustainability Report P.4

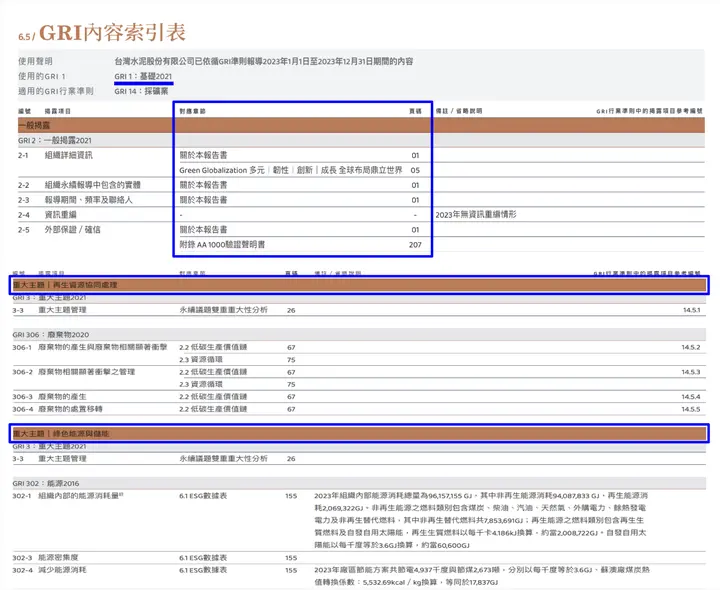

(2) Not Using GRI Standards Index

Common Deficiency: Not using GRI Standards Index, or not including material topics in the GRI Standards Index. Additionally, material topic content must be fully disclosed in the report.

Better Disclosure Practice: Compile a GRI Standards Index in the report appendix, clearly indicating the corresponding chapters and page numbers for each indicator. GRI 2-1 to 2-5 are mandatory disclosure items that cannot be omitted; if other GRI 2 series indicators are not disclosed, specific reasons for omission must be provided.

For example: If a company has no GRI 2-4 restatement situation, it is recommended to clearly indicate "No information restatement this year" in the index, rather than simply omitting the indicator.

Additionally, for material topics, companies need to comprehensively list corresponding GRI topic standards and ensure the report specifically discloses each indicator with corresponding content locations.

Report Example:

Source: Taiwan Cement 2023 Sustainability Report P.190, 193

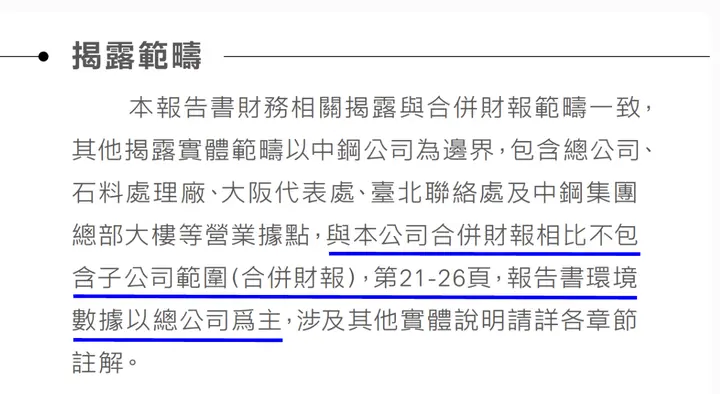

(3) Not Explaining Inconsistency with Financial Report Disclosure Scope (GRI 2-2)

Common Deficiency: Not explaining differences between sustainability report disclosure scope and subsidiaries included in consolidated financial statements.

Better Disclosure Practice: Clearly explain differences between disclosure scope and consolidated financial report scope. For example, if Company A's consolidated financial report covers all subsidiaries while the sustainability report only covers headquarters, it should clearly state "Subsidiaries not included in disclosure scope," or provide a "Consolidated Financial Report Link" as in the example below for stakeholders to access.

Report Example:

Source: China Steel 2023 Sustainability Report P.1

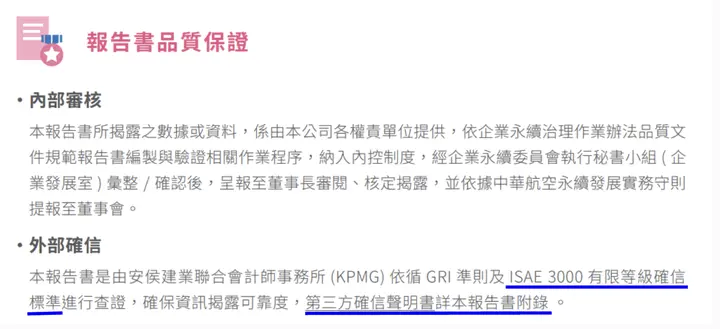

(4) Not Indicating Third-Party Assurance Status (GRI 2-5)

Common Deficiency: Not indicating whether various disclosed content has been subject to third-party assurance.

Better Disclosure Practice: If the report has undergone external verification or assurance, companies must clearly explain the assurance institution, standards and levels adopted, and provide links to the assurance report or statement.

Report Example:

Source: China Airlines 2023 Sustainability Report P.5

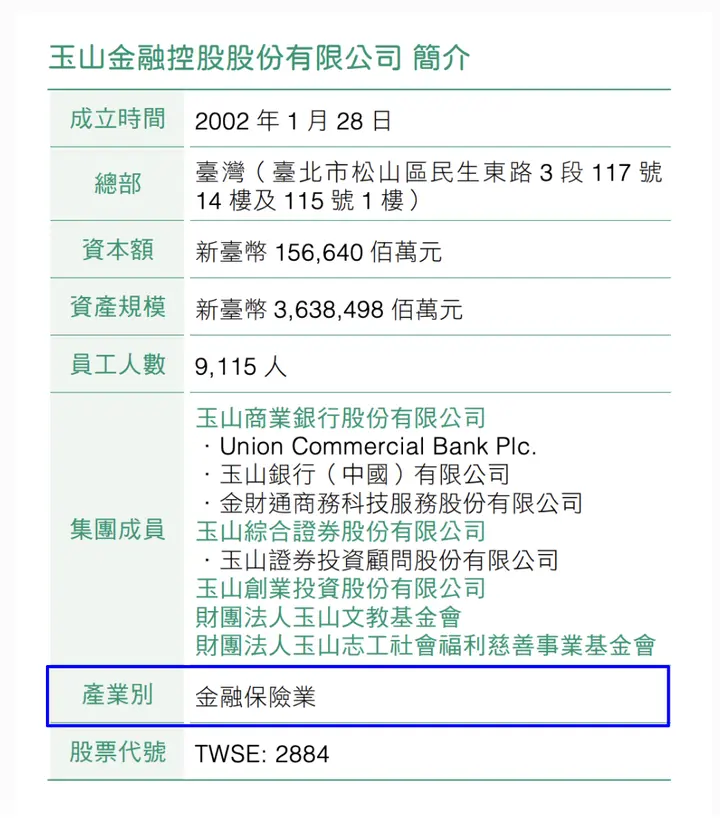

(5) Not Disclosing Industry Classification (GRI 2-6)

Common Deficiency: Not disclosing the company's industry classification in the report

Better Disclosure Practice: Refer to TWSE industry classifications to clearly state the company's industry classification in the report.

Report Example:

Source: E.SUN FHC 2023 Sustainability Report P.14

(6) Not Disclosing Employment Type Distribution and Headcount Changes by Region (GRI 2-7)

Common Deficiency 1: Not disclosing full-time, part-time, or other employment types by region

Better Disclosure Practice: Companies can categorize employees by company locations and present the number of employees by full-time, part-time, and other employment types.

Report Example:

Source: IRCE 2023 Sustainability Report P.108

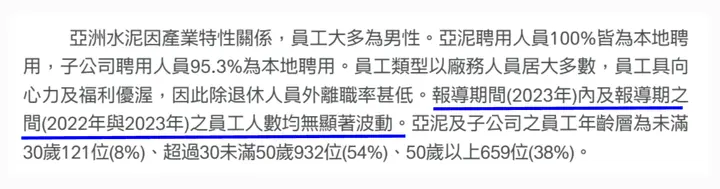

Common Deficiency 2: Not disclosing significant fluctuations in employee numbers during the reporting period compared to the previous year

Better Disclosure Practice: If the company's employee numbers significantly changed compared to the previous year, explain the change and reasons; if no significant fluctuation, clearly disclose "No significant fluctuation in employee numbers" rather than omitting without explanation.

Report Example:

Source: Asia Cement 2023 Sustainability Report P.87

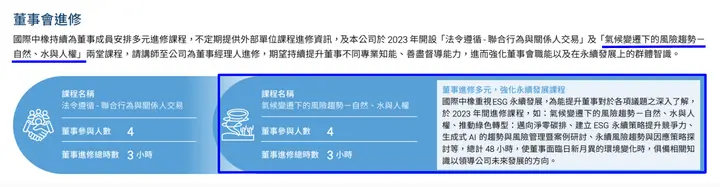

(7) Not Disclosing Board ESG Competency Enhancement (GRI 2-17)

Common Deficiency: Not disclosing board ESG training or other practices to enhance board ESG competency.

Better Disclosure Practice: Explain whether board members have participated in ESG-related courses through training, seminars, or professional development; if so, describe the content and hours to meet this indicator requirement.

Report Example:

Source: IRCE 2023 Sustainability Report P.26

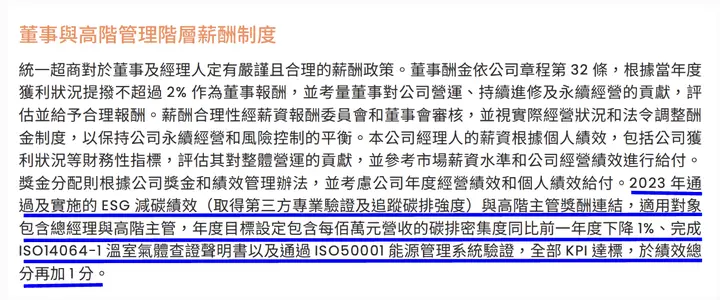

(8) Not Disclosing Executive Compensation Link to Sustainability Goals (GRI 2-19)

Common Deficiency: Not disclosing remuneration policies for highest governance body and senior management, and not explaining how their compensation is related to company sustainability goals and performance.

Better Disclosure Practice: Explain items linking senior executive compensation to environmental, social, or governance performance, supplementing with proportion, evaluation methods, and relationship to sustainability goals. If no such linkage exists, clearly disclose "Currently the company has not linked compensation to sustainability goals" rather than omitting.

Report Example:

Source: Uni-President 2023 Sustainability Report P.45

(9) Not Disclosing Annual Total Compensation Ratio Indicators and Omission Reasons (GRI 2-21)

Common Deficiency: Formula errors, not disclosing GRI 2-21 annual total compensation ratio, and not explaining reasons for omission.

Better Disclosure Practice:

Companies need to disclose the following two items:

- Ratio of "highest-paid individual's annual total compensation" to "median annual total compensation of all other employees"

- Ratio of "highest-paid individual's annual total compensation change rate" to "median annual total compensation change rate of all other employees"

Note: When calculating "median annual total compensation change rate of all other employees," first calculate each employee's compensation change rate, then derive the median from these values, rather than directly comparing the salary median of two years.

Report Example:

Source: Formosa Plastics 2023 Sustainability Report P.126

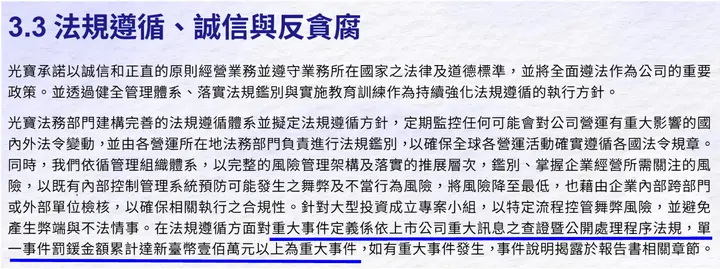

(10) Not Explaining Significant Violation Event Criteria (GRI 2-27)

Common Deficiency: Not defining "significant violation events" and not explaining the basis and evaluation criteria for judgment

Better Disclosure Practice: Explain company's criteria for defining "significant violation events," for example: According to listed company material information verification and disclosure procedures regulations, a single event with cumulative fines reaching NT$1 million or above constitutes a significant violation event.

Report Example:

Source: Lite-On Technology 2023 Sustainability Report P.46

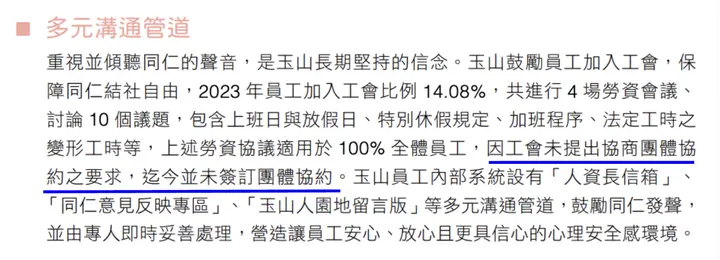

(11) Not Explaining Collective Bargaining Agreement Status and Employee Protection Measures (GRI 2-30)

Common Deficiency: Not explaining reasons for not signing collective bargaining agreements, or not describing protection measures or alternative arrangements for employees not covered by collective bargaining agreements.

Better Disclosure Practice: (For companies without unions or with unions but no collective bargaining agreement):

Explain reasons for not signing collective bargaining agreements, such as no union established yet, union has not proposed, etc., and supplement with protection mechanisms or alternative measures for employee working conditions to address labor rights protection needs.

Report Example:

Source: E.SUN FHC 2023 Sustainability Report P.146

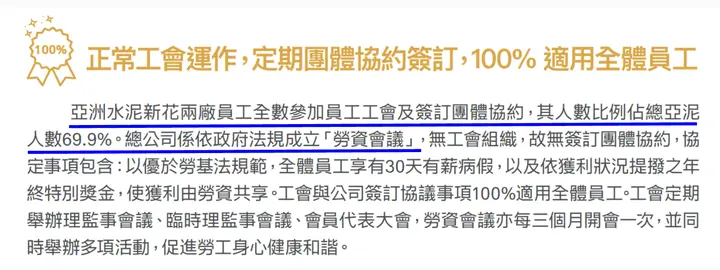

Better Disclosure Practice: (For companies with collective bargaining agreements):

Explain the scope and employee coverage ratio of collective bargaining agreements, and supplement protection measures for working conditions of employees not covered to ensure all employees receive basic rights protection.

Report Example:

Source: Asia Cement 2023 Sustainability Report P.93

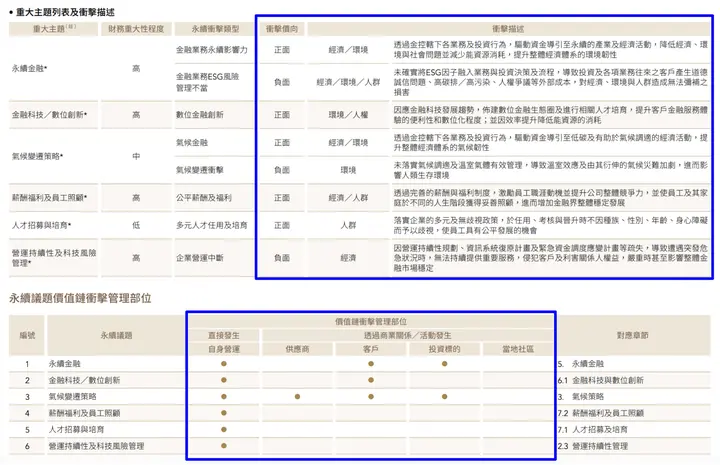

(12) Not Disclosing Impact Scope of Material Topics (GRI 3-3)

Common Deficiency: Not disclosing the actual impact scope of material topics on internal and external parties.

Better Disclosure Practice:

Explain the positive and negative impacts of material topics on economy, environment, and society, indicate whether impacts are directly caused by company operations or from upstream/downstream value chain, and describe main operational activities in the value chain.

Report Example:

Source: Taishin FHC 2023 Sustainability Report P.24, 26

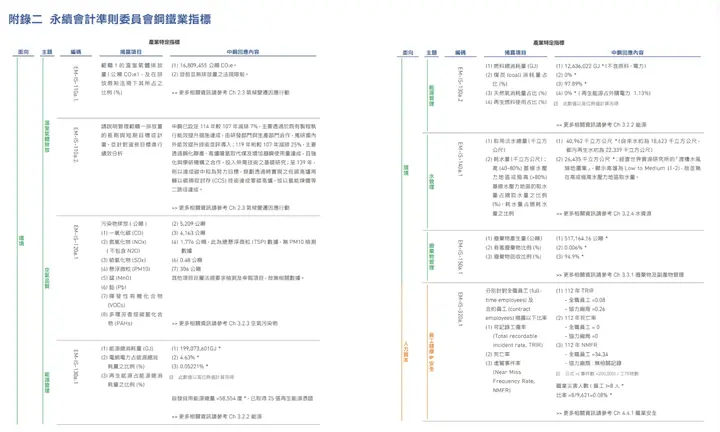

(13) Not Disclosing Industry Sustainability Indicators

Common Deficiency: 14 specific industries need to disclose additional sustainability indicators. Failure to include an index table in the appendix will be listed as a deficiency.

Better Disclosure Practice: Disclose corresponding sustainability indicators based on specific industry classification, and compile an index table in the report appendix indicating disclosure locations for each indicator to enhance information completeness and accessibility.

Report Example:

Source: China Steel 2023 Sustainability Report P.154

Strengthening Sustainability Information Internal Controls: Starting from Systematic Management

Regulatory authorities regularly review sustainability reports to ensure disclosed information has quality, consistency, and traceability. As disclosure requirements become increasingly stringent, preparation methods using Word and Excel make it difficult to manage data sources and lack change records, easily leading to data errors, information inconsistency, or unclear accountability.

Therefore, many companies have adopted digital system tools that use permission settings, version control, and approval workflows to improve preparation efficiency while strengthening information transparency and compliance, helping companies establish sustainability information internal controls.

Sustaihub Syber Sustainability Management System has three key features that help companies ensure sustainability information accuracy:

- History tracking, approval workflows: Improve data reliability

- Cross-departmental data integration and real-time updates: Solve data fragmentation issues

- Multi-level permission controls: Strengthen sustainability information and data security

Through Syber Sustainability Management System helps companies achieve compliance and improve internal efficiency without requiring extensive manpower and time, providing comprehensive support for sustainable development as the best sustainability report collaboration platform.

👉 Apply for trial now Syber Sustainability Management System, start your digital sustainability journey

Through digitalization, AI, and cloud integration, Syber Sustainability Management System helps you transcend traditional limitations, making your sustainability reports more persuasive and better able to demonstrate corporate spirit, becoming your assistant in promoting sustainable development.

Source: Corporate Governance Center Review Mechanism and Common Deficiencies